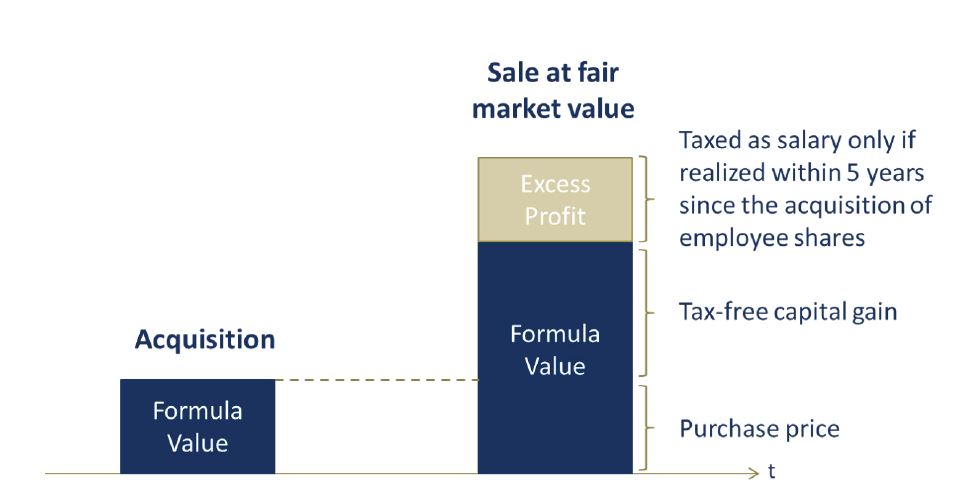

Under the current tax framework, the non-uniform cantonal tax practices on the capital gains treatment and valuation of employee shares lead to different tax consequences for employees depending on their place of residence. The experts from Walder Wyss review the update of Circular Letter No. 37 on the taxation of employee shareholdings. In the piece, they provide background for if you are not familiar with the topic; along with information for the valuation of non-listed employee shareholdings; taxation upon the acquisition of the employee shares; taxation upon the disposal of the employee shares; founder shares; and employee shares acquired at third- party conditions.

Read the full article here.